Jack Scoville

Jack Scoville is an often quoted market analyst in the grain and soft commodities sectors. You will find his commentary throughout the Reuters, Wall Street Journal, Dow Jones, Bloomberg, and Barron's publications. Contact Mr. Scoville at (312) 264-4322

Weekly Ag Markets Update – 04/13/2026

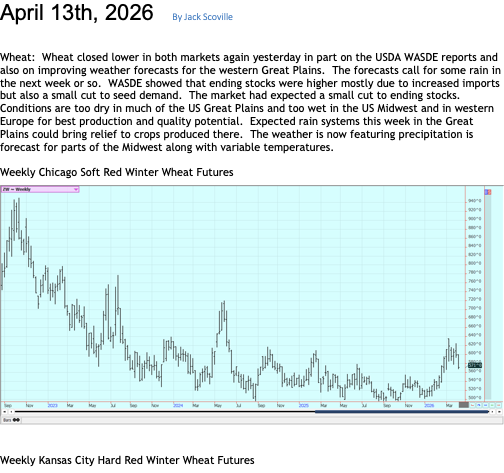

Wheat: Wheat closed lower in both markets again yesterday in part on the USDA WASDE reports and also on improving weather forecasts for the western Great Plains. The forecasts call for some rain in the next week or so. WASDE showed that ending stocks were higher mostly due to increased imports but also a small cut to seed demand. The market had expected a small cut to ending stocks. Conditions are too dry in much of the US Great Plains and too wet in the US Midwest and in western Europe for best production and quality potential. Expected rain systems this week in the Great Plains could bring relief to crops produced there. The weather is now featuring precipitation is forecast for parts of the Midwest along with variable temperatures.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Kansas City Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

Unavailable today

Corn: Corn was lower last week as the weather is good in the US and early planting is expected. Early planting traditionally leads to large yields. The WASDE reports made no changes to Corn and was considered neutral for prices. There are still excessive supplies as seen in the recent USDA reports after prices were trending higher on strong demand. Temperatures in the Midwest should be generally warm for the next week. Conditions are called good in Argentina and big production is expected there. Oats were lower and trends are mixed on the daily charts and mixed to on the weekly charts as the market held support areas.

Weekly Corn Futures

Weekly Oats Futures

Soybeans and Soybean Meal: Soybeans and Soybean Meal were higher last week as the weather for planting is good in the US. Soybean Oil was lower The WASDE report increased the domestic crush by 35 million bushels but cut exports by the same amount to leave ending stocks unchanged. The US government apparently has no idea on how to manage risks in the Hormuz or how to end the war. Big South American crops are being harvested, and ideas are that Chinese buying could be interrupted due to the Iran war and new import rules imposed by China. South American sources said that the Brazil crops are now more than 65% harvested. The tariff wars between the US and other countries add to cost of US Soybeans. Temperatures will be generally warm in the Midwest for the next week.

Weekly Chicago Soybeans Futures

Weekly Chicago Soybean Meal Futures

Rice: Rice closed lower last week and trends are turning down on the daily and weekly charts. The market failed at resistance on the weekly charts. Trends are still up on the daily charts after a big war related rally with the war with Iran and the political problems with China not having much effect on prices. Traders anticipate less production this year in the US and around the world due to low prices. USDA said that Rice planted area would be about 12% less in the coming year. Demand remains moderate for US Rice.

The U.S. rice outlook for 2025/26 projects steady supplies, lower domestic use, reduced exports, and higher ending stocks. Domestic use and residual is lowered by 2.0 million cwt to 169.0 million, all long-grain, primarily on the latest NASS Rice Stocks report which indicated less December-February disappearance than previously estimated. All rice exports are reduced by 3.0 million cwt to 82.0 million, also all long-grain, on continued slow sales and shipments to Western Hemisphere markets. Ending stocks are increased by 5.0 million cwt to 55.3 million, the highest since 1985/86. The 2025/26 season-average farm price (SAFP) for all rice stays at $12.10 per cwt with offsetting changes. The long-grain SAFP is lowered by $0.10 per cwt to $10.40, while the medium- and short-grain SAFP for Other States is raised $0.50 per cwt to $14.70.

This month’s global rice forecast for 2025/26 is for higher supplies, lower consumption, reduced trade, and increased ending stocks. Supplies are up by 0.4 million tons to 732.9 million, largely due to greater production in Thailand. Consumption is lowered by 0.4 million tons to 540.6 million, reflecting changes in several countries. Trade falls by 0.5 million tons to 61.5 million, mainly because of a reduction for Pakistan on its slow export pace. As a result of these changes, global ending stocks are raised 0.8 million tons to 192.3 million.

Weekly Chicago Rice Futures

Vegetable Oils: Palm Oil futures was lower last week as the Iran war keep bio fuels demand hopes active but mixed and Crude Oil futures and other petroleum markets weaker. Demand ideas are in a state of flux right now due to the war. Canola was lower last week.

Weekly Malaysian Palm Oil Futures

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures

Cotton: Cotton was higher last week despite ideas of improving weather for the western Great Plains and desert southwest. The WASDE reports showed no significant changes. The market is worried about the weather that remains hot and dry in US Cotton areas, mostly from Texas to the west, but forecasts are now calling for some showers in the region. Overseas production in places like India and Brazil are expected to be high, but overall world production is expected by USDA to fall on reduced global planted rea and reduced yields. Trends are mixed to down on the daily charts.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: Futures were slightly higher last week in response to the USDA reports and on demand reports The reports showed that US production at 61.6 million boxes and Florida production at 12.2 million boxes. Trends are turning up on the daily charts. The Florida harvest is about over and isolated showers are now being reported. The weather for the next crop is dry but seasonal and some rains are starting to appear. Chart trends are mixed on the daily charts. The weather is considered good for production in Brazil and Mexico. Scattered showers are still reported in Brazil.

Weekly FCOJ Futures

Coffee: New York and London were both a little lower yesterday. There are still ideas of good supplies available on the farm, but getting Coffee from the farm to the market is another problem due to the war with Iran. Brazil said exports might not improve that much in March due to shipping costs and concerns. There are reports of very good conditions in Brazil and a large crop is forecast. Brazil producers have stopped selling due to the recent fall in prices. World production conditions are generally good. Scattered showers are being reported now to improve tree condition in Brazil. Mexico is in good condition, as is Central America. Vietnam has scattered showers lately and conditions there are called good.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: New York was a little higher and London was lower last week. The war has increased world petroleum prices and could divert demand from Sugar production to production of ethanol. But some in the market expect less war in the near future. India, the world’s second-largest producer, had no plans to curb sugar exports to provide downward pressure on prices. Trends are mixed on the daily charts in both markets. There are good supplies for the market from good growing conditions for cane and beets around the world. The prospect of a big global surplus in the 2025/26 season was keeping the market on the defensive but a rise in production in India and Thailand being offset by the war

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

Cocoa: New York and London closed near unchanged last week. Short term trends are mixed in both markets. A big main crop harvest has arrived in West Africa and rains have been positive for the next crop. There are still reports of increased production potential in other countries outside of West Africa, including Asia and Central America. The market feels that there is less demand due to the high prices seen last year and the lack of demand is expected to continue. Weak demand has led to a build-up on unsold supplies in both Ivory Coast and Ghana, while the prospect of another global surplus in 2026/27 are real. Cocoa demand has fallen sharply after prices nearly tripled in 2024, prompting chocolate makers to reformulate ingredients and shrink the size of their bars. Cocoa arrivals at ports in top grower Ivory Coast since the start of the season on October 1 reached 1.445 million tons by April 5, up 0.2% from the same period last season,

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

Questions? Ask Jack Scoville today at 312-264-4322